Several commodity markets are poised for well-defined up-trends this year. I plan to write about these markets on a regular basis as the views presented here are more thematic and longer term in nature. Updates to the trading strategies published here will be provided on an ongoing basis. In this issue, I will be focusing Corn and Sugar

This is the first issue of the Commodity Newsletter that I have written in some time. I hope to continue to publish this newsletter every two weeks as the themes in the Commodity markets I track tend to be thematic and longer term in nature.

With potential for a Fed Rate Cut this week, a Brexit deal, a China Tariff deal, peaceful resolutions in Hong Kong and the Middle East. Any and all of these issues can spark buying in Commodities. With the current fund traders net short as of the last COT report in Corn, Meal, Wheat, Copper, Coffee, Cotton and Natural Gas, we could see a squeeze play out in any of these commodities as we see resolutions of the global issues mentioned. It is important to note that index funds have been buyers of commodities in the last few weeks.

The ultimate resolution of the China Tariff situation may be many months away as intellectual property and other issues may still be unresolved by December 15th; but consider that the agricultural buying could jump $40 billion in the next few years if tariffs are dropped.

The Corn crop is of major interest as some major producing states are going to see the end of their season before full maturity. I am long Corn and in profit and holding the trade as the Corn market should continue to climb into the 450s by year end. Combine this with a trade deal and China buying Corn for their Ethanol usage and we could see a nice squeeze into year end. Sugar is of particular interest this week as the Real rallied last week and has pressed prices higher; a reversal is in progress into $14. I am waiting on a confirmation on Lean Hogs as we are in the peak production season now and near lows. China is purchasing Hogs as their agricultural crisis continues as mentioned in previous issues of the Commodity Advisory Newsletter.

Please see the past issues of the Commodity Advisory Newsletter for more information on the China Tariff situation and commodities covered here on The Art of Chart.

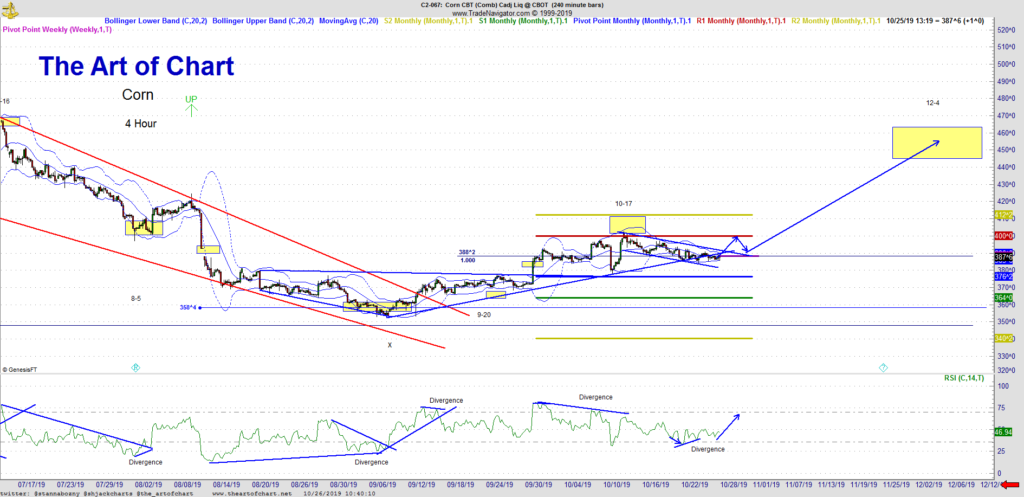

Corn

The Corn market is going to have lower acreage and lower yields this year. The October freeze damage was enough to push yields down to 165 bushels per acre. As of the last Crop Report, maturity was at 85% which is behind the average of 97%, Michigan 62% mature, North Dakota 65%, South Dakota 74% and Wisconsin 61%. Some prime growing area will see their season end before full maturity. If we get a China Trade deal, expect the wide difference between US and China Corn to close rapidly.

Looking at the Charts, technically we have seen the retest as expected into 385 and the next rally requires a break of $391 to break the flag channel and opens $410 next. Looking for a December price in Corn of $450.

Trading Strategy

I currently have a December Corn position, the 380/430 Call Spread and I may juice it with March futures on a break and conversion of 394. If you are not in the position, you could start a longer dated position on Corn by buying the March futures at 394 or a simple call spread the March 400/450.

Sugar

There has been a large supply surplus in Sugar of over 9 million tonnes in 2018 and until now, not much has changed in the fundamentals. Sugar fundamentals have been bearish for some time but they could shift bullish. The graphic below shows global production in metric tons for 2018 with Brazil the leading producer in the world. Thailand is expected to come up short by about 10%. This means that unless something changes we are likely going to see a global production deficit of 3 million tonnes.

Last week, we were looking for a reversal in Sugar and the Brazilian Real supported Sugar prices with a rally. It appears that Sugar has reversed and the four hour chart below shows that we have positive divergence on RSI and are through the timing window. A break of the Monthly Pivot, the blue line, should yield a rally into $14.00. The daily chart shows a nice setup using the COT report with commercials net long and funds and retail net short. I am expecting a rally into December according to my price and timing work of $14.00.

Trading Strategy

I want to give myself some time on this trade and am considering an entry in March. In March, consider buying Sugar at 12.18 and risk no more than 30 ticks.

Wrap Up

These trades are posted on our private twitter feed and further discussed each week on The Weekly Call which can be found HERE.

I will continue to cover thematic trades in the commodity world in this newsletter. My next newsletter will be in two weeks and will likely focus on the Soft sector. Until then, Trade Smart and Trade Safe.

Disclaimer: Trading futures contracts and commodity options involves substantial risk of loss, and may not be appropriate for all investors. By reading this report, you acknowledge and accept that all trading decisions are your sole responsibility. Trading strategies referenced in this document are only suggestions, no representation is being made that they will achieve profits or losses. Past performance is no guarantee of future results.

27th Oct 2019

27th Oct 2019