Paragon Options is a service that focuses exclusively on futures options. By doing so we are taking advantage of superior premiums compared to stock options and asset diversification offered by futures. Paragon Options is a directional options service that will focus on Metals, Energies, Bonds, Currencies, and Commodities. This service will launch on June 25th.

A Long S&P 500 Futures Options Trade

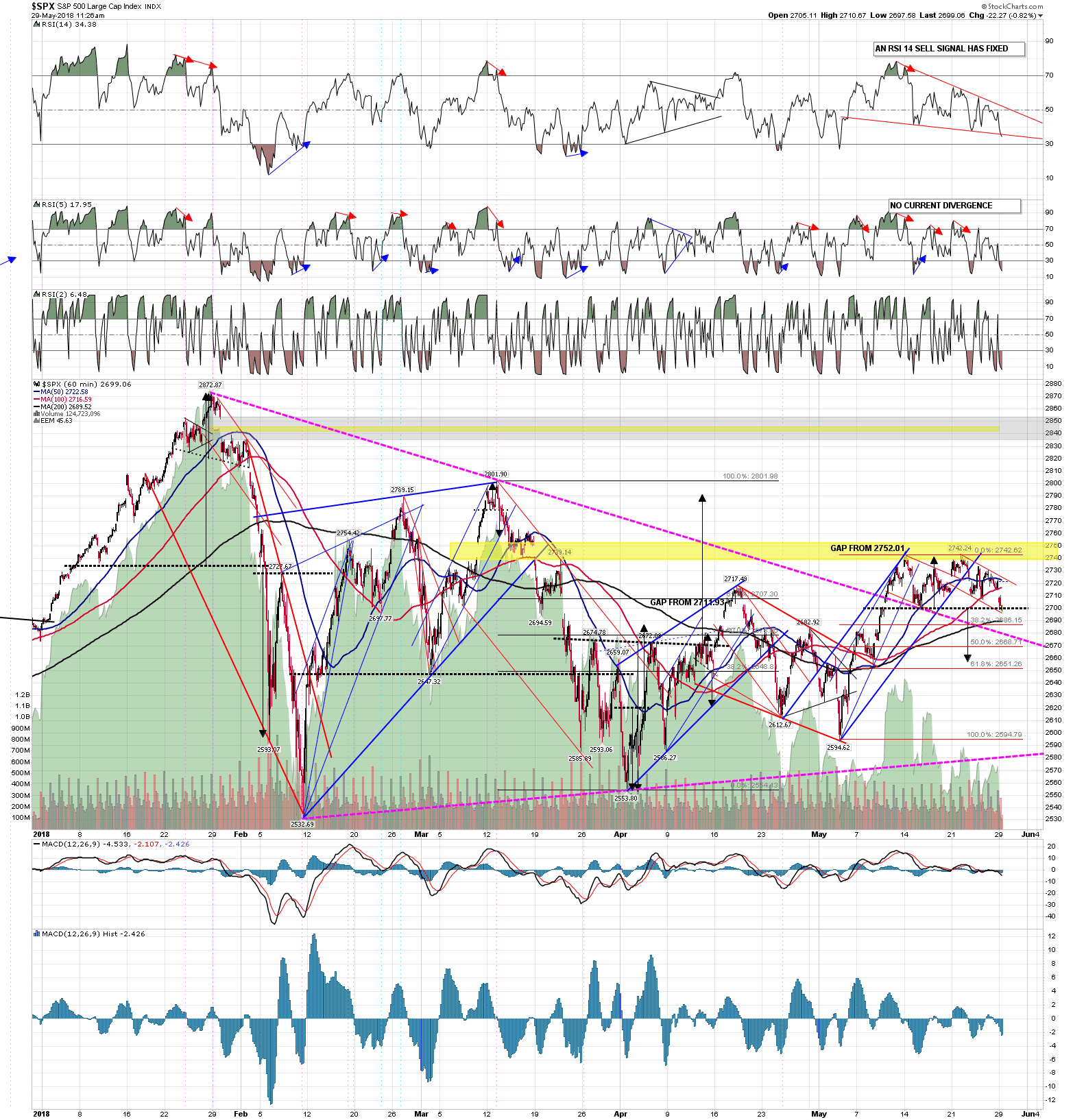

In the short term, the S&P 500 futures (ES) had broken up from a triangle and we were expecting a retest of 2760-70 before any significant further downside. At the time of writing that working assumption is being tested.

The downside risk at 2675 on the S&P 500 is at a second backtest of broken declining/triangle resistance. A break below opens a double top target in the 2661.50 area, and potentially a test of rising support from the February low, now in the 2580 area. SPX 60min chart:

S&P 500 Futures Options Risk reversal

We are expecting a quick rise to around the 2770 level by the June futures option expiry (15th June) in the S&P 500 Emini Future (ES). This trade is current and live as of now. It was opened on the 15th May with the underlying price of ES future at 2707 (vs Jun). Our risk on this trade is 2675, and we will be looking to add on any dips.

Long Jun 2750 Call vs Short 2650 Put (Risk reversal)

We have opened a risk reversal in futures options on ES by buying a Jun 2750 call and selling a 2650 put against it. This trade is known as a risk reversal and they are usually set up for close to zero cost. In this instance, we set up the trade for a credit of $4.50.

Both the legs of this trade are bullish and the deltas must be added together giving us a total delta of 59 or 59% of a future. This futures option trade has the capability of increasing to 100 delta or 1 future which is a near doubling of its initial exposure.

To see why we took this particular strategy, we need to have a look at the vol skew.

This is a graph of the current vol skew in ES futures options. This is a typical looking skew for equities. You will note that the out of the money puts are much more expensive than the out of the money calls. The reason for this is mentioned in the free webinar we did which if you missed can be found here.

With equities, as the underlying rises, the vol will usually collapse and vice versa. This is important to be aware of when constructing trades. Had we for example just bought ATM or OTM calls, and been right in our prediction of direction, we would have had a loss of value from a vol crush to contend with.

By using a risk reversal, we had a nearly flat exposure to volatility (Vega) and in fact, as the put had more vega than the call, an upward move in the underlying would mean we make money from the volatility falling.

This position also benefits from time decay as the short put has more value than the call and so the passage of time ticks in our favor currently.

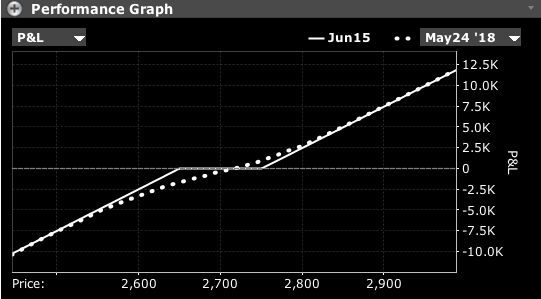

Here is the P&L profile of the position.

You will note that both upside and downside on the position is unlimited, and so from a risk perspective the trade has to be monitored carefully with a strict adherence to exiting at 2675 should we be wrong.

If you look at the solid line you can see the expiry day profile of this position. In short, should the market be between 2650 and 2750 at the expiry, the whole trade will drop out worthless and we will simply collect the setup credit of $4.50. The dotted line follows the P&L as it would move today at the time of writing.

Summary

This trade is currently sitting at $-9.90 with ES futures at 2693 as I am writing and so we are slightly offside but still well within our risk parameters. We will report any further adds or exits should either of those arise.

Yet again, this is a new and different type of strategy than the ones we have previously used as we custom build all of our trades from scratch taking into account all of the necessary variables.

29th May 2018

29th May 2018